Latest

The state of online retail

UK eCommerce is hard hit right now, down c.5% YoY after Q1 according to IMRG. There is some relief likely to come in H2 2024, kicked off by a Summer of Sport and latterly with a general election which has been preceded by tax cuts.

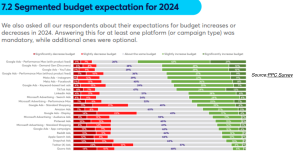

Health and Beauty and Sports and Outdoor are the categories most likely to drive growth in UK retail, while Clothing and Electronics will remain in negative territory through the year. Total online sales are being impacted by less disposable income, the resurgence of stores and 7-8% fewer people heading online to shop, which creates a perfect storm for those with a big annual sales target to hit online.

Go on tell me, how bad is it?

What can I say about retail right now that hasn’t already been said? On first glace very little – year on year the online market is significantly down, in an extended recession in all but name. Total revenue is down c.5% according to IMRG, with some categories such as Fashion faring even worse. Looking at the consistent trend, there is little relief on the horizon and we can expect more of the same in Q2 until inflation is back at 2% target and interest rates are cut. In saying that, April will be more interesting as a result of the latest cut to National Insurance and Easter washing through.

It can’t be all bad news though?

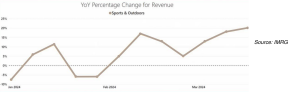

Hmmm not all bad I suppose. If you look at the trends, consumers are keener than ever to be healthy, active and more glamorous. Health and Beauty remains the standout category, with only five weeks this year not seeing revenue growth vs the previous year. Sports and Outdoor are also showing signs of life in 2024 and this positive revenue growth is expected to continue for the year and rise on the back of our Summer of Sport with both the Euro football and the Olympics this summer.

So why is retail so challenging right now?

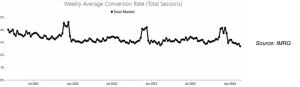

Primarily it is disposable income, or the lack of it. Consumers are either spending all their money on bigger energy and service bills or they’re stuffing their savings in a bank account where interest rates outstrip inflation. The knock on effect is fewer customers shopping and despite what Google says, less online traffic, which IMRG reports is down -5% over the last 12 months. This is compounded by a 20% fall in conversion rate across UK eCommerce in the last 3 years that is still yet to bottom out. Lastly we are also seeing stores steal the sales share of online again – the first time in twenty years!

How are marketers getting more with less?

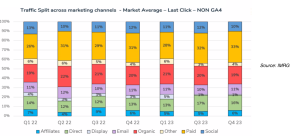

Interestingly there is a clear move to prioritise paid media, whose share of last click traffic is up 10% YoY. This is likely driven by two factors:

1.FDs wanting immediate trackable sales – paid has always been a safe haven for budgets and ROI and during hard economic times it’s always a channel that is protected internally

2.Google, Meta and Amazon’s relentless push to prioritise paid media, driving up CPCs, total ad revenues and the share price.

If you go one level deeper you can see the impact Google’s ‘feed-based’ Performance Max campaign type is having on paid advertising, with 63% of practitioners expecting to increase P-Max budget at the expense of Display and X, formerly known as Twitter.

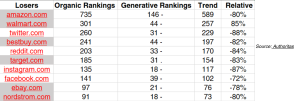

We can see Google’s new search generative experience is also particularly penalising retailers, with six of the top ten traffic losers made up of retailers in the US.

Recommendations

- Keep the budget tight until Summer, matching or shaving off a few % points to push into H2

- If you’ve got stores, use them as your superpower and drive ‘footfall’ with specific campaigns such as ‘Store Goals’ and ‘Lead Generation’

- Fight the urge to put every penny into paid activity and develop a broad and robust channel mix across paid, earned and owned. You will reap the benefits in the long term.

- Implement the latest tech to lower costs and increase reach. Working with a Comparison Shopping Service and having effective Feed Management such as ‘Productcaster’ is critical for squeezing every penny. Renegotiating you affiliate platform provider is also a great way to lower BAU costs.

- Manage up, using insights from Google, IMRG, ONS, Similar Web, Authoritas, GFK you can understand market share, consumer behaviour and business performance.

References

https://www.ons.gov.uk/businessindustryandtrade/retailindustry/timeseries/j4mc/drsi

https:/www.theguardian.com/business/2012/jun/27/uk-retail-sales-strong-jubilee-cbi

https:/tradingeconomics.com/forecast/consumer-confidence

Ready for change? Let's talk

Speak to Summit